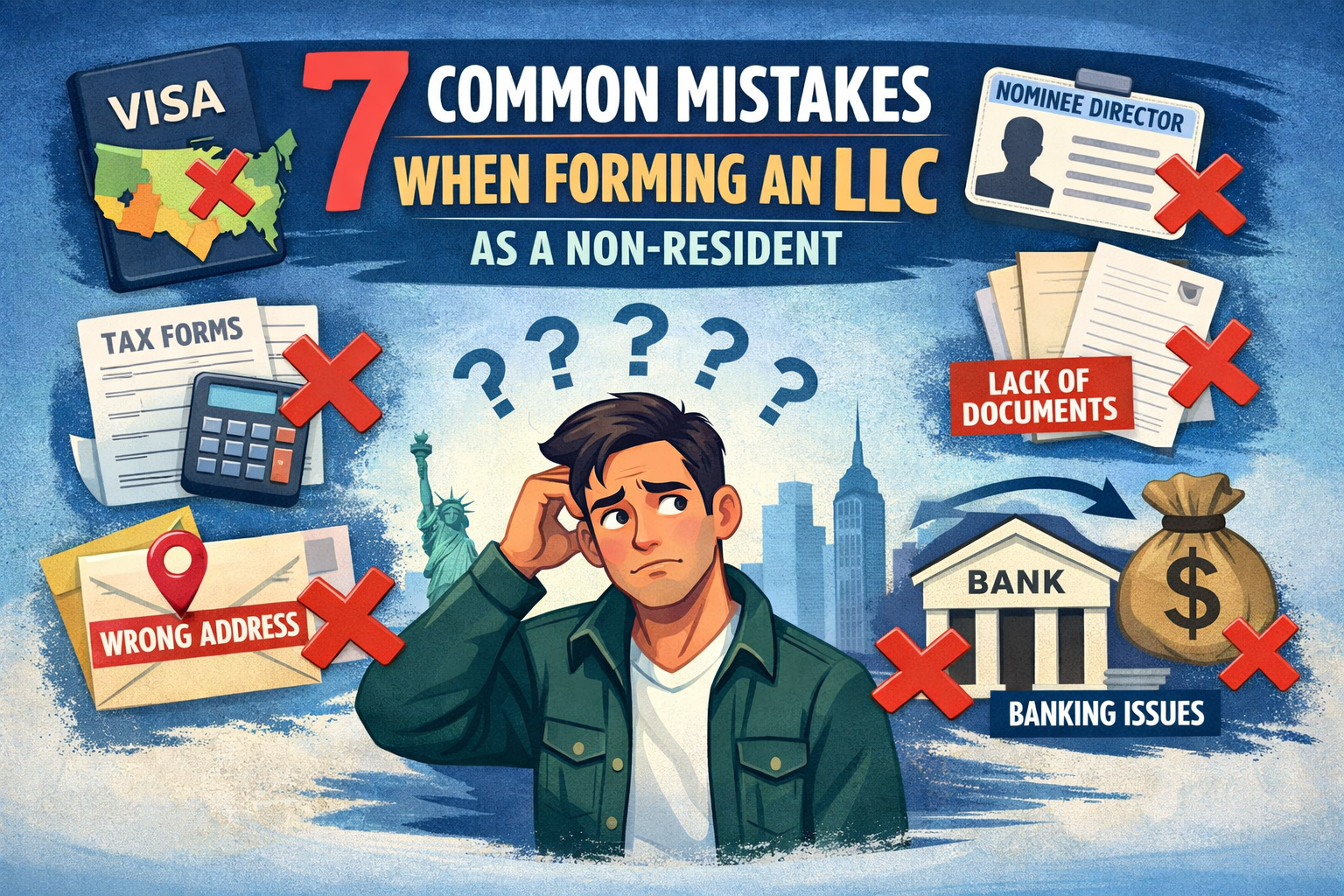

7 Common Mistakes When Forming an LLC as a Non-Resident and How to Avoid Them

Forming a limited liability company as a non-resident can be a significant step toward entering the U.S. market and expanding your global business. However, many non-resident entrepreneurs encounter pitfalls during the process that can lead to unnecessary costs, legal trouble, or missed opportunities. Understanding these mistakes and how to avoid them is critical to safeguarding your personal assets and ensuring your business success.

Whether you’re looking to protect your business reputation, minimize tax implications, or comply with complex U.S. tax laws, knowing the right procedures is essential. By addressing these common mistakes and planning accordingly, you can navigate the requirements with confidence and maximize the advantages of forming a U.S. LLC.

The Basics of Forming a Limited Liability Company in the United States

Why LLCs Are Popular Among International Entrepreneurs

A limited liability company (LLC) offers a flexible and straightforward way for international entrepreneurs to establish a business in the United States. One of the key reasons LLCs are so popular is the liability protection they provide. Unlike a sole proprietorship, where the owner’s personal assets are at risk, an LLC separates personal and business liabilities, offering robust asset protection. This structure ensures that in case of legal disputes or debt, only the business assets are at risk.

In addition to liability protection, LLCs are favored for their adaptable legal structure, making them ideal for small businesses and online businesses. The LLC model allows you to manage the business in a way that best fits your business needs, whether you run it as a single-member LLC or involve multiple partners. Moreover, LLCs offer greater privacy protections compared to other business types, as the names of members are often not publicly disclosed in certain states.

For international entrepreneurs, forming an LLC also opens doors to the U.S. market, allowing access to a large consumer base and a well-established legal framework. Whether you’re launching a global business or targeting a niche market, an LLC can be the right structure to support your growth.

LLC vs. Sole Proprietorship and Other Business Entities

Choosing between an LLC and a sole proprietorship is one of the first decisions non-resident entrepreneurs face. A sole proprietorship is simpler to set up, but it lacks the liability protection that an LLC provides. This means that your personal assets, such as your home or savings, could be at risk in case of business debts or lawsuits. On the other hand, an LLC ensures that your personal and business liabilities remain separate, providing essential legal protections.

Comparing LLCs to other business entities like C corporations and S corporations, the differences become more nuanced. C corporations often involve double taxation, where income is taxed at both the corporate and shareholder levels. S corporations, while avoiding double taxation, have stricter eligibility requirements and limitations on the number of shareholders. LLCs, by contrast, offer tax flexibility, as they can be taxed as a sole proprietorship, partnership, or corporation depending on the business type and tax planning strategy.

Additionally, single-member LLCs differ from multi-member LLCs in terms of management and tax reporting requirements. While single-member LLCs are simpler to manage, they require compliance with specific tax forms like Form 5472 for reporting transactions with foreign owners. Multi-member LLCs, though slightly more complex, allow for shared management and broader business operations.

Choosing the Right State for Your U.S. LLC

How to Avoid the Costly Mistake of Picking the Wrong State

One of the biggest mistakes non-resident LLC owners make is choosing the wrong state for their company formation. Each state has its own tax rates, filing requirements, and annual fees, which can significantly impact the overall cost of running your LLC. States like California, for instance, impose high annual fees and additional taxes, making them less favorable for those looking to minimize costs. On the other hand, states such as New Mexico are popular for their low-cost structures and privacy protections, making them an attractive option for foreign entrepreneurs.

When choosing the right state, you should also consider your specific business operations and tax implications. If your LLC will have a physical address or conduct significant business in a particular state, you may be subject to that state’s tax rules, including state income tax and sales tax. Conducting thorough research or consulting a tax advisor can help you identify a state that aligns with your business needs and minimizes hidden costs.

Ultimately, picking the wrong state could lead to unnecessary expenses, legal trouble, and compliance issues. It’s crucial to evaluate factors such as annual fees, tax obligations, and filing requirements before making a decision. The right state can provide a solid foundation for your U.S. LLC and ensure it remains in good standing.

How State Tax Laws and Tax Treaties Affect Non-Resident Entrepreneurs

For non-resident entrepreneurs, understanding state tax laws and tax treaties is essential to avoid costly mistakes. State taxes can vary significantly, with some states imposing no state income tax, while others have high rates. Additionally, some states require LLCs to collect and remit sales tax, which could add complexity to your tax reporting obligations.

Tax treaties between the United States and your home country may also influence the tax benefits you receive. These treaties can help you avoid double taxation and provide opportunities for tax savings, depending on the provisions in place. However, the interaction between U.S. tax laws and international tax rules can be complicated, so consulting a tax professional is highly recommended to ensure compliance and maximize tax advantages.

Being aware of state-specific tax rules and leveraging applicable tax treaties can make a significant difference in the financial viability of your LLC. Proper tax planning will not only minimize your liabilities but also position your business for long-term success.

Understanding Tax Obligations and Tax Reporting Requirements

Essential Tax Forms and Procedures for Non-Resident LLC Owners

Non-resident LLC owners must familiarize themselves with U.S. tax obligations and ensure compliance with tax reporting requirements. One of the first steps is obtaining an Employer Identification Number (EIN) by filing IRS Form SS-4. The EIN is necessary for opening a U.S. bank account, filing tax forms, and conducting business operations legally in the United States.

Single-member LLCs owned by non-U.S. residents are required to file Form 5472 to report transactions between the LLC and its foreign owner. This form is crucial for maintaining compliance with the Internal Revenue Service (IRS) and avoiding penalties. Multi-member LLCs, on the other hand, must file additional forms based on their tax classification, whether as a partnership or corporation.

In addition to federal tax requirements, you may also need to handle sales tax and self-employment taxes depending on your business model. Sales tax obligations apply if your LLC sells taxable goods or services in the United States, while self-employment taxes may be applicable if you’re actively involved in the business. Ensuring accurate and timely tax reporting is essential to avoid fines and maintain your LLC’s good standing.

Why Tax Planning and Consulting a Tax Professional Is Crucial

Tax planning is a critical aspect of forming and managing an LLC as a non-resident. Without proper guidance, you risk overlooking important tax implications that could result in hidden costs or compliance issues. A qualified tax professional can help you navigate the complexities of U.S. tax laws, identify tax savings opportunities, and ensure that your LLC complies with all federal and state regulations.

Consulting a tax advisor is especially important for understanding how tax treaties, tax rates, and deductions can affect your LLC’s profitability. They can provide tailored tax advice that aligns with your home country’s tax rules and your business operations. By investing in professional tax planning, you can mitigate risks, optimize your tax benefits, and focus on growing your U.S. company without unnecessary stress.

Legal Documents and Filing Procedures for LLC Compliance

Filing Articles of Organization and Staying in Good Standing

Filing the Articles of Organization is the foundational step in forming an LLC in the United States. This document outlines essential details about your LLC, such as its name, physical address, and the registered agent’s contact information. Filing requirements vary by state, so ensuring accuracy and compliance with state-specific procedures is crucial to avoid delays or legal trouble. Many states allow for online submission, making it the easiest way to get started with your new company.

Maintaining your LLC’s good standing involves more than just initial filing. States typically require annual reports and fees to keep your LLC active and compliant. Missing deadlines for these filings could result in penalties or even the dissolution of your LLC. Regularly monitoring your compliance obligations and setting reminders for key deadlines will help protect your business reputation and liability protection.

In addition to annual reports, maintaining proper records of your LLC’s legal documents is essential. This includes operating agreements, tax filings, and minutes of any official meetings. Keeping these documents organized ensures you’re prepared for audits or legal inquiries, providing peace of mind as your business grows.

Meeting Deadlines to Avoid Legal Trouble

Deadlines are a critical aspect of staying compliant with U.S. regulations. Late filings or missing forms like Form 5472 or state-specific tax forms can lead to hefty fines and jeopardize your LLC’s good standing. For instance, the Internal Revenue Service imposes significant penalties for failing to file required forms on time, which can be particularly burdensome for non-resident LLC owners.

To avoid legal trouble, consider working with compliance professionals or using specialized services that help monitor filing requirements. These resources can ensure that your LLC meets deadlines for annual reports, state taxes, and federal tax obligations, allowing you to focus on your business operations. Proactive compliance not only avoids fines but also strengthens your LLC’s legal protections and credibility with investors and partners.

Opening a U.S. Business Bank Account and Address Requirements

How a U.S. Bank Account Supports Business Operations

Opening a U.S. business bank account is a vital step for any non-resident entrepreneur forming an LLC. A U.S. bank account simplifies financial transactions, making it easier to pay vendors, receive payments from U.S. customers, and manage operating expenses. It also establishes credibility with clients and partners, showcasing your commitment to conducting business within the United States.

Having a dedicated business bank account helps separate personal and business finances, which is essential for maintaining liability protection. This separation ensures that your LLC remains a distinct business entity, safeguarding your personal assets in case of legal disputes. Additionally, a U.S. bank account facilitates tax reporting by providing clear records of your LLC’s income and expenses, simplifying the process of filing annual reports and tax forms.

However, opening a U.S. business bank account can be challenging for non-resident LLC owners due to requirements like a physical address and an Employer Identification Number. Many banks also ask for a Social Security Number, which non-us residents typically do not have. Researching banks that cater to international entrepreneurs or using specialized services can help you navigate these hurdles and successfully open an account.

Step-by-Step Guide for Non-Resident Entrepreneurs

To open a U.S. business bank account, start by obtaining your LLC’s Employer Identification Number (EIN) from the Internal Revenue Service by filing IRS Form SS-4. This EIN acts as your LLC’s tax identification number and is mandatory for account opening. Next, you’ll need to provide proof of your LLC’s formation, such as a copy of the Articles of Organization and any state-specific registration certificates.

Some banks may require a physical address in the United States to open an account. If your LLC does not have a U.S. office, consider using a registered agent or a virtual office service that provides a compliant address. Once you’ve gathered all the necessary documents, schedule an appointment with a bank that specializes in working with non-resident entrepreneurs. Some banks even allow remote account opening, which can simplify the process for international entrepreneurs who cannot travel to the United States.

By following these steps and ensuring you meet the bank’s requirements, you can successfully open a U.S. business bank account. This will provide a solid foundation for your business operations, helping you manage finances, build credibility, and streamline compliance with U.S. tax laws.

Maximizing Opportunities While Avoiding Legal and Tax Issues

Forming an LLC in the United States as a non-resident presents numerous opportunities, but success depends on careful planning and compliance. Choosing the best state for your business model, such as one with low fees or favorable tax rates, can set your LLC up for long-term success. Additionally, leveraging tax advantages and tax savings opportunities through proper tax planning can maximize your LLC’s profitability.

Following a strong legal framework not only attracts venture capital but also ensures compliance with U.S. regulations, helping you avoid legal trouble. Whether you’re entering the U.S. market for online business, real estate investments, or other ventures, a well-structured LLC can serve as a gateway to your global business ambitions.